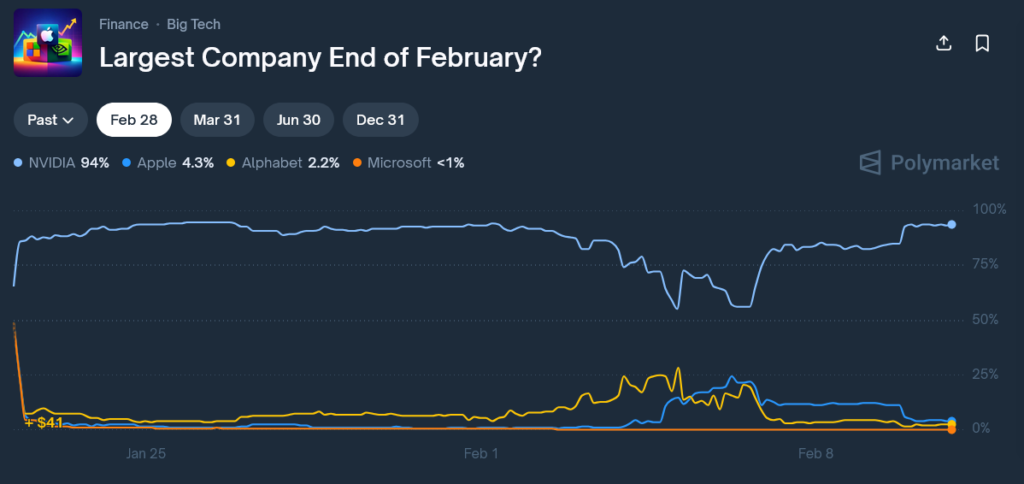

NVIDIA holds a near-certain 99% probability to end February as the world’s largest company by market capitalization on Polymarket. The AI chipmaker currently trades at 98.9¢ on the YES outcome, reflecting an almost unanimous market consensus in its ability to maintain its commanding valuation lead through the final week of February.

With NVIDIA’s market cap at $4.61 trillion as of February 21, 2026, versus Apple’s approximately $3.84 trillion, traders are pricing in just a 1% chance that any rival could close the gap by month end.

This market has generated total volume of $11.53 million, with NVIDIA’s odds now locked at the ceiling of 99% as the distance between the top two companies has stretched well beyond $700 billion.

Notably, Apple is no longer even the second largest company. Alphabet surpassed Apple’s market cap in January 2026 for the first time since 2019, meaning Apple has fallen to third place in the global rankings.

The shift reflects a broader recognition that NVIDIA’s dominance in AI infrastructure has created a structural advantage that short term market volatility cannot easily erase.

NVIDIA’s market cap has grown by nearly 49% over the past 12 months, while Apple faces analyst headwinds including a Raymond James downgrade signaling that substantial growth in 2026 may be difficult to achieve.

Meanwhile, Alphabet’s aggressive pivot into AI, fueled by the success of Gemini and a 65% stock surge in 2025, has fundamentally reshuffled the global market cap leaderboard beneath NVIDIA.

Last updated: February 21, 2026 — This article has been refreshed with the latest Polymarket odds, current market cap data, and corrected catalysts ahead of NVIDIA’s Q4 FY2026 earnings on February 25, 2026. Original analysis published February 9, 2026.

Largest Company by the End of February?

This Polymarket event tracks which publicly traded company traders believe will be the world’s largest by market capitalization at the end of February. Odds reflect expectations around earnings, stock momentum, macro conditions, and sector leadership.

Disclosure: This link may be an affiliate link. I may earn a commission at no extra cost to you.

Market Overview: The 94% Consensus

The Polymarket event “Largest Company End of February?” presents a clear hierarchy of outcomes based on which company will have the highest market capitalization at the close of trading on February 28, 2026:

Current Odds (as of February 21, 2026):

- NVIDIA: 98.9¢ (99% probability), up 23 percentage points from its recent low

- Apple: 0.79¢ (1% probability)

- Alphabet: 0.64¢ (1% probability)

- Microsoft: 0.36¢ (less than 1%)

- Tesla: 0.30¢ (less than 1%)

- Amazon: 0.26¢ (less than 1%)

- Saudi Aramco: Under 0.25¢ (less than 1%)

The odds have evolved dramatically since the market opened, with NVIDIA surging to a near-certain 99% after recovering from a sharp DeepSeek-driven tech selloff in late January 2026 that briefly sent sentiment lower.

With NVIDIA’s earnings report due on February 25, 2026 as the only remaining major catalyst, and the company sitting on a $700 billion plus market cap lead over second place Alphabet, traders have effectively closed the debate.

This corporate valuation market has proven far more directional than typical event-driven markets. NVIDIA has not traded below 90% probability since recovering from the late January selloff, and the current 99¢ ceiling reflects a market that sees no credible near term path for any competitor to close a lead that now exceeds 15% of NVIDIA’s own market cap.

Historical precedent supports this stability: top-spot market cap flips between multitrillion-dollar companies have historically required either a catastrophic company specific shock or weeks of sustained underperformance, neither of which materialized for NVIDIA in February.

What This Market Is Asking

This market resolves based on which publicly traded company holds the highest market capitalization at the close of U.S. trading on February 28, 2026. Market capitalization is calculated as stock price multiplied by total outstanding shares, with data sourced from major financial data providers including Bloomberg, Reuters, and Companies Market Cap.

The baseline as of February 19 to 20, 2026 shows NVIDIA at approximately $4.57 to $4.62 trillion, Alphabet at approximately $3.94 trillion, and Apple at approximately $3.84 trillion. A critical update from the old baseline: Alphabet surpassed Apple’s market cap in January 2026 for the first time since 2019, meaning the #2 threat to NVIDIA’s crown is now Alphabet, not Apple.

NVIDIA currently holds approximately a $630 billion lead over second place Alphabet. For the outcome to flip, Alphabet would need to gain roughly 16% while NVIDIA holds steady, or NVIDIA would need to fall approximately 13.8% while Alphabet holds flat.

The bar is even higher for Apple, which sits $730 billion behind NVIDIA and would need to surge nearly 19% in the final seven days of February to take the top spot.

The resolution source remains market cap data published by established financial data aggregators on March 1, 2026, based on closing prices from February 28. No rounding or edge cases apply since market cap is calculated to the exact dollar, though in practice movements of less than $10 billion are statistically insignificant for companies at this scale.

With only 5 trading sessions remaining and NVIDIA’s earnings on February 25 as the sole remaining macro catalyst, the resolution window is extremely narrow.

Why “NVIDIA” Is the 94% Favorite?

NVIDIA commands an estimated 90 to 97% share of the global AI accelerator market, with its Blackwell architecture GPUs sold out through at least mid-2026 and a backlog of 3.6 million units already committed to hyperscale customers.

The Blackwell GPU line has not just succeeded Hopper. CEO Jensen Huang called Blackwell sales “off the charts” and confirmed cloud GPUs are fully sold out on the company’s Q3 FY2026 earnings call.

The company reported record revenue of $57.0 billion in Q3 FY2026 (quarter ended October 26, 2025), representing 62% year over year growth, while EPS surged 67% to $1.30, beating analyst consensus of $1.26.

Data Center revenue alone reached $51.2 billion, up 66% year over year, and accounted for nearly 90% of total sales. NVIDIA has also guided Q4 FY2026 revenue at $65 billion (plus or minus 2%), a figure that, if confirmed on February 25 earnings, would represent yet another record quarter.

This growth trajectory dramatically outpaces Apple’s most recent quarter. Apple posted record Q1 FY2026 revenue of $143.8 billion, up 16% year over year, with EPS of $2.84 beating estimates, driven largely by a holiday iPhone surge and services growth. While Apple’s quarter was impressive, 16% revenue growth and a hardware-heavy mix stand in sharp contrast to NVIDIA’s 62% top-line growth and its pure-play AI infrastructure positioning.

TSMC’s advanced packaging capacity for CoWoS and HBM3E memory integration continues to constrain Blackwell supply, reinforcing NVIDIA’s pricing power and gross margin expansion.

NVIDIA’s non-GAAP gross margin held at 73.6% in Q3 FY2026, with guidance for 75% in Q4, creating a structural moat that is difficult for any rival to replicate through mid-2026

China Market Reopening and $50 Billion Opportunity

CEO Jensen Huang announced in January 2026 that NVIDIA is experiencing “very high” demand from Chinese customers for H200 AI chips, which the U.S. government recently approved for export.

Huang estimated this market could reach $50 billion annually, representing incremental revenue not included in NVIDIA’s existing $500 billion two year forecast. The H200 chips have resumed production and are moving through NVIDIA’s supply chain, with export license finalization underway.

While Bernstein projects NVIDIA’s China market share will decline from 66% to 54% by 2025 due to domestic competition, the absolute size of the Chinese AI infrastructure market is expanding so rapidly that even a smaller share translates to significant revenue growth.

The recent approval provides a competitive advantage over the 12 to 18 month period when H200 sales were blocked.

Stock Performance and Valuation Resilience

NVIDIA shares surged 7.78% on February 6, 2026, marking their best single day performance since April, as investors bought the dip following a tech sector selloff. The stock has gained 32.21% over the past year, with the company’s market cap expanding from $3.5 trillion to $4.62 trillion.

This growth rate significantly exceeds Apple’s 19.25% annual increase, which has been insufficient to close the valuation gap.

Despite concerns about gaming GPU delays due to memory chip shortages, these constraints actually reinforce NVIDIA’s strategic decision to prioritize high margin AI chips over consumer graphics cards.

The Blackwell architecture underpins both data center GPUs and the current RTX 50 series gaming products, with the next generation Rubin chips planned for late 2026 targeting 3.3 times Blackwell’s speed.

Why “Apple” Is Only 4%?

The Hardware Revenue Plateau and Growth Deceleration

Apple’s iPhone shipments tell a very different story in 2025 than the old article suggested. Far from declining, Apple shipped a record 247.8 million iPhones in full year 2025, up 6.3% year over year, driven by the iPhone 17 series.

In Q4 2025 alone, Apple led all smartphone vendors globally with 81.3 million units shipped, a 4.9% gain year over year and its best Q4 growth since 2021. The old claim of a 5% iPhone shipment decline applies to calendar Q4 2024, not current data, and no longer holds as a bearish argument.

The more accurate bear case rests on the scale of Apple’s valuation gap relative to NVIDIA. Apple posted record Q1 FY2026 revenue of $143.8 billion, up 16% year over year, with EPS of $2.84, up 19%, and generated nearly $54 billion in operating cash flow in the quarter.

Impressive as those numbers are, 16% revenue growth is dwarfed by NVIDIA’s 62% year over year growth in its most recent quarter, and Apple’s gross margin of 47.3% TTM is less than two thirds of NVIDIA’s 73.6% non-GAAP gross margin. The structural gap in growth rate, not a hardware cycle slowdown, is the real reason Apple cannot close the distance.

With NVIDIA’s market cap lead over Apple sitting at approximately $730 billion as of February 21, 2026, Apple would need to surge nearly 19% in the final 5 trading sessions of February while NVIDIA stays flat.

IDC also flags a potential headwind on the horizon: Apple may postpone the base iPhone 18 model to 2027, breaking its traditional annual release cycle and risking a 4.2% shipment decline in 2026. That forward uncertainty further limits any valuation re-rating argument for Apple in the near term.

Services Growth Insufficient to Drive Near Term Revaluation

While Apple’s services segment overtook iPhone as the largest contributor to gross profit in Q4 2025, with Apple Intelligence Pro subscription priced at $9.99 per month attracting 20% of Pro model users, this recurring revenue stream takes years to materially impact total company valuation.

Analysts project that AI driven services monetization could add billions in recurring revenue by 2027, but the February 28, 2026 resolution date arrives too soon for these initiatives to close the current valuation gap.

The partnership with Google to power Siri 2.0 using Gemini technology represents a strategic pivot, but also highlights Apple’s lag in proprietary AI model development compared to NVIDIA’s infrastructure dominance.

While these collaborations support Apple’s long term positioning, they do not change the near term reality that Apple lacks a catalyst strong enough to drive 14.6% outperformance versus NVIDIA in just 18 trading days.

Valuation Multiple Compression Risk

Apple’s price to earnings ratio reflects expectations for steady but unspectacular growth, while NVIDIA’s elevated P/E ratio of 46 is justified by earnings per share growth projections of 50% compared to Apple’s 22%.

For Apple to overtake NVIDIA by month end would require either a significant NVIDIA specific negative catalyst such as a major customer cancellation or regulatory action, or an Apple specific positive surprise such as a transformative product announcement, neither of which appears imminent based on current information.

The January 2026 dynamic where NVIDIA briefly traded below Apple before reasserting dominance demonstrates that traders view Apple’s windows of opportunity as temporary rather than sustainable trends. Each time Apple narrows the gap through positive momentum, NVIDIA’s underlying revenue growth and margin expansion reassert the valuation differential within weeks.

Key Catalysts to Watch

- NVIDIA Q4 FY2026 Earnings (February 25, 2026, 5:00 PM ET): Consensus expects $65 billion in revenue and EPS of $1.53. The real mover will be Q1 FY2027 guidance, with expectations near $75 billion. Options markets are pricing in a plus or minus 8 to 10% post-earnings move.

- FOMC Minutes (Already Released, February 19, 2026): The Fed signaled a “hawkish pause” with no imminent rate cuts, pushing the 10-year Treasury yield toward 4.1% and applying broad pressure on high-multiple tech stocks.

- China Export Controls (Active Downside Risk): China blocked NVIDIA’s H200 chips in January 2026. China’s share of NVIDIA’s AI chip revenue has dropped to zero. Any diplomatic resolution before February 28 is a positive wildcard, but no timeline exists.

- Blackwell Supply Chain: CoWoS packaging and HBM3E memory constraints remain the key production bottleneck. Any update at the February 25 earnings call on GB300 ramp capacity could shift NVIDIA’s forward valuation.

How to Trade This Market?

Strategy 1: Straight NVIDIA YES (Low Risk)

Action: Buy NVIDIA YES at 94¢

Thesis: The $590 billion market cap cushion provides massive downside protection, requiring either a 12.8% NVIDIA decline or 14.6% Apple rally in 18 trading days to flip the outcome

Return: 6.4% total return (approximately 130% annualized over 18 days)

Risk: Catastrophic NVIDIA specific event such as Blackwell architecture flaw discovery, major hyperscaler cancellation, or unexpected China export ban reversal

Strategy 2: Apple NO Arbitrage (Low Risk)

Action: Buy Apple NO at 96¢ (implied from 4¢ YES price)

Thesis: Apple would need to outperform NVIDIA by 14.6 percentage points in under three weeks, requiring unprecedented momentum shift given recent trends

Return: 4.2% total return (approximately 85% annualized)

Risk: Surprise Apple product announcement or major NVIDIA production halt creates short term volatility window for outcome flip

Strategy 3: Fade the Field Multi Leg (Medium Risk)

Action: Sell Google/Alphabet/Microsoft YES at aggregate 3¢ while buying NVIDIA YES at 94¢ for diversified downside hedge

Thesis: For any company besides NVIDIA or Apple to win requires both NVIDIA and Apple to collapse simultaneously by 20%+, an extraordinarily unlikely scenario

Return: 3% premium collection on field bets plus 6.4% on NVIDIA position if held to expiry

Risk: Black swan market crash event that disproportionately impacts NVIDIA and Apple while sparing Alphabet or Microsoft, though correlation makes this highly unlikely given tech sector dynamics

The Verdict

NVIDIA’s 99% probability reflects a simple mathematical reality: its approximately $730 billion lead over Apple and $630 billion lead over second place Alphabet cannot be closed in 5 remaining trading sessions without a catastrophic company specific shock. No plausible scenario flips this market before February 28.

The fundamentals back the odds. NVIDIA posted 62% year over year revenue growth, holds 73.6% non-GAAP gross margins, and is guiding to $65 billion in Q4 FY2026 revenue, with analyst consensus near $75 billion for Q1 FY2027. The only live risk is the February 25 earnings call, where options markets are pricing in a plus or minus 8 to 10% move that could briefly compress the gap.

Buying NVIDIA YES at 98.9¢ returns 1.1%, annualizing to roughly 57% over 7 days. The dollar return is modest at this stage, but the near-zero risk makes it a clean capital-efficient trade.