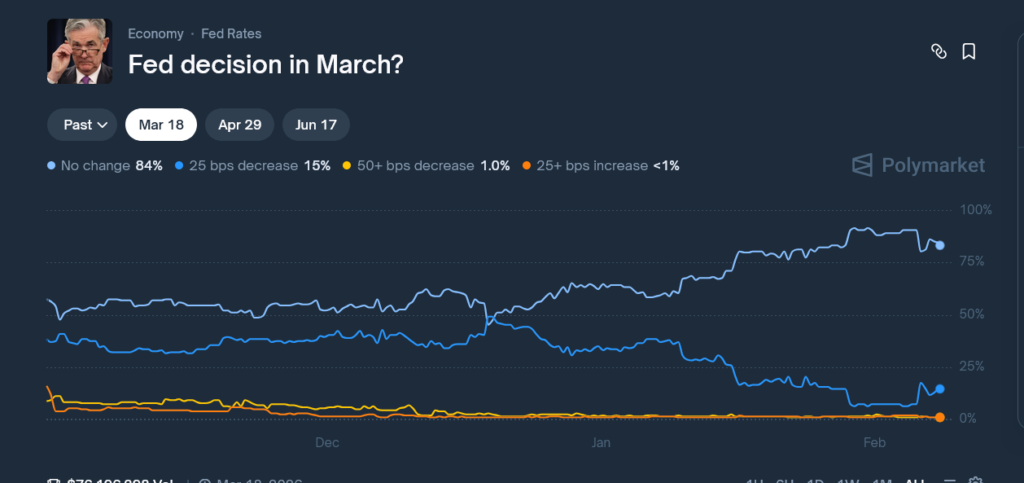

Will the Federal Reserve change interest rates at its upcoming March 17-18, 2026 meeting? Polymarket traders have delivered a clear verdict: most likely NO.

“No Change” shares are currently trading at 83.5¢ (83.5% probability) versus 14.5¢ for a 25 bps cut, 1.1¢ for 50+ bps cut, and under 1¢ for hikes, with total volume exceeding $1.2 million across brackets.

The market reflects a firm consensus for holding rates steady at 3.75%-4.00%, a shift from early-year expectations of three cuts in 2026 now down to just two projected total.

Fed Decision in March?

This Polymarket event tracks what traders believe the Federal Reserve will decide at the March meeting. Odds reflect expectations around rate cuts, rate holds, or surprise moves based on inflation data, labor market strength, and evolving macroeconomic conditions.

Disclosure: This link may be an affiliate link. I may earn a commission at no extra cost to you.

Market Overview: The 83.5% Hold Consensus

Current pricing shows strong but not unanimous confidence in stability. “No change” leads at 83.5% probability, with cuts totaling about 16% and hikes negligible.

- 25 bps decrease: Trades at 14.5¢ (14.5% probability).

- 50+ bps decrease: Priced at 1.1¢ (1.1% probability).

25+ bps increase: Under 0.5¢ (<0.5% probability). The “No change” odds have climbed from around 70% in late January to the current 83.5% level amid resilient data.

Total volume across March brackets has hit $1.2 million, making this one of Polymarket’s most liquid Fed markets for 2026.

What This Market Is Asking?

This market resolves based on the upper bound of the target federal funds rate after the March 2026 FOMC meeting.

Current Target: 3.75%-4.00%.

Resolution Source: The FOMC’s official statement (Expected March 18, 2:00 PM ET).

The Nuance: Changes are rounded to the nearest 25 bps bracket (e.g., a 12.5 bps cut rounds to 25 bps). The event covers multiple contracts for precise outcomes like no change, 25 bps down, 50+ bps down, or 25+ bps up.

Why “No Change” Is the 83.5% Favorite

1. Economic Data Supports Patience

Inflation has cooled to 2.7% YoY CPI, nearing the Fed’s target but still requiring confirmation of sustainability. November payrolls added 227K jobs, unemployment holds at 4.1%, and Q3 2025 GDP grew 3.0% annualized.

Wage growth remains steady at 3.8% YoY, balancing inflation risks without signaling distress. This “soft landing” mix justifies a pause before further easing.

2. Fed Guidance Emphasizes Data Dependence

Powell reiterated a “wait-and-see” approach in recent speeches, noting robust jobs data offsets cooling inflation.

The December 2025 Dot Plot projected only two 25 bps cuts for all of 2026 (down from three), implying a terminal rate near 3.75%-4.00% by mid-year.

FOMC minutes highlighted fewer cuts amid strong GDP, aligning with market repricing.

3. Broader Stimulus and Growth Dynamics

Fiscal tailwinds from 2025 policies continue boosting Q1 2026 demand, competing with monetary easing goals. Robust GDP at 3% and stable financial conditions reduce cut urgency.

Why Rate Change Scenarios Are Only 16%

The Case Against a 25 bps Cut (14.5%)

Core PCE at 2.6% and housing inflation up 3.2% YoY keep pressure on. Cutting now risks reacceleration, especially with payrolls at +227K. Analysts note data “raises the bar” for March action.

The Case Against 50+ bps Cut (1.1%)

Requires sharp labor deterioration (e.g., unemployment >4.5%) or credit stress, neither evident. This tail risk suits hedges only.

The Case Against a Hike (<0.5%)

4% GDP growth supports it economically, but post-2025 cuts, it would erode credibility amid political scrutiny.

Key Catalysts to Watch

- February CPI/PCE (Early March): Below 2.5% YoY could lift cut odds to 25%+.

- February Payrolls (Early March): Under +150K shifts hold odds below 75%.

- FOMC Statement (March 18, 2:00 PM ET): “Persistent inflation” language reinforces pause.

- Powell Press Conference (March 18, 2:30 PM ET): Dot Plot revisions will guide 2026 path.

How to Trade This Market?

Strategy 1: Consensus Hold (Moderate Risk)

Action: Buy “No Change” YES at 83.5¢ or better.

Thesis: Data alignment (2.7% CPI, 227K jobs, 3% GDP) matches Fed patience.

Return: ~20% if holds (240% annualized to resolution).

Risk: Soft data surprise.

Strategy 2: Cut Convexity Play

Action: Buy 25 bps decrease YES at 14.5¢.

Thesis: Faster disinflation or market stress reprices to 30%+ probability.

Return: 6x potential.

Risk: High if data stays firm.

Strategy 3: Tail Hedge (Low Allocation)

Action: Buy 50+ bps YES at 1.1¢.

Thesis: Black swan like labor shock.

Return: 90x potential.

Risk: Near-certain loss probability.

The Verdict

83.5% “No change” odds are well-supported by 2.7% CPI, 227K payrolls, 3% GDP, and Powell’s data-dependent stance projecting just two 2026 cuts.

This market offers parking for hold bulls or convexity for cut skeptics. Post-March, watch Q2 contracts for the next repricing battle. Trade via Polymarket.